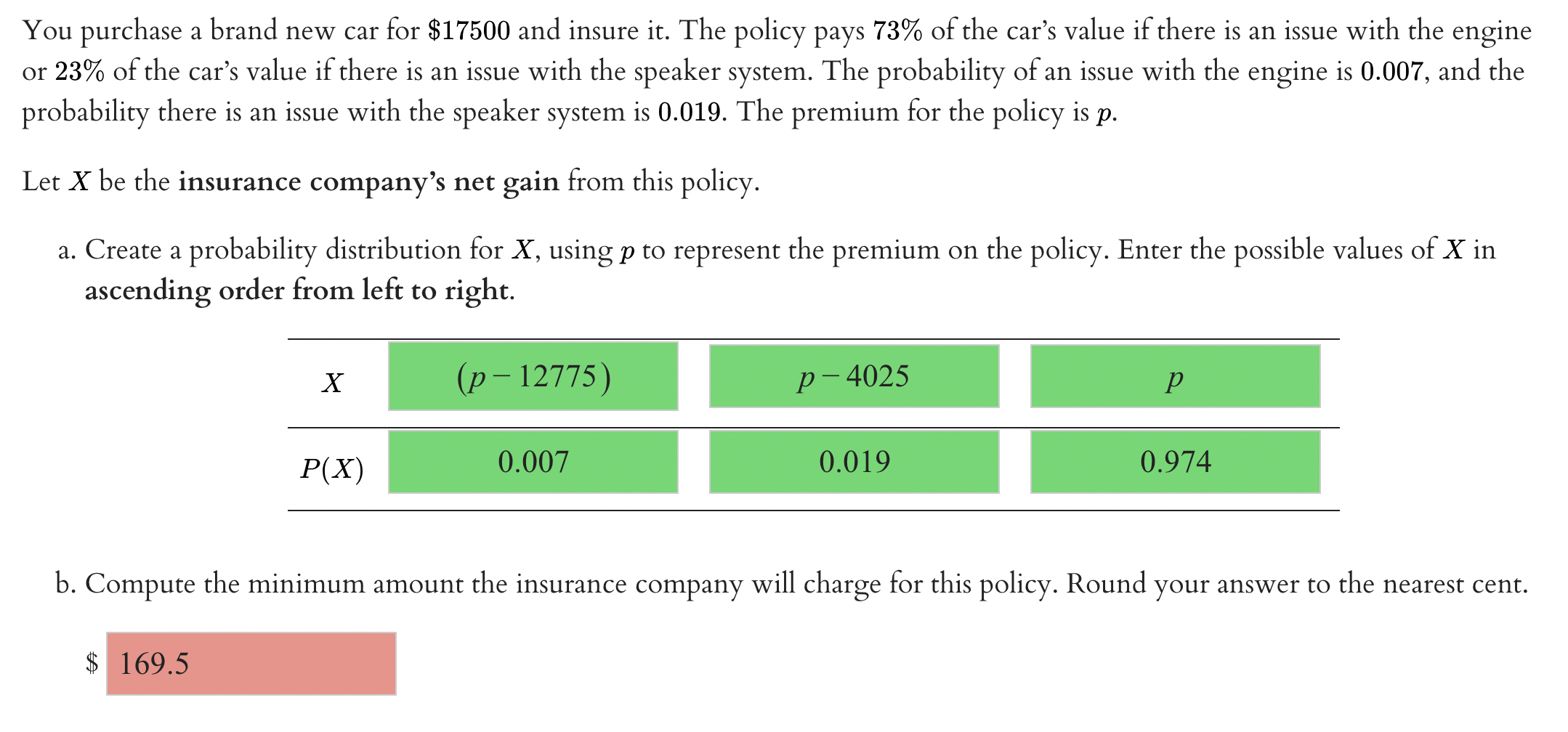

Second mortgages can be found in a couple first variations: house security finance and you can household guarantee personal lines of credit (HELOCs)

Determining whether or not to make use of the security of your home to repay unsecured debt and you will/otherwise create renovations might be a difficult monetary choice. The opportunity of lowest yearly percentage prices and smooth monthly installments makes next mortgage loans extremely glamorous. Although not, utilizing your family to have guarantee try a decision that needs to be considered very carefully.

Household Collateral Loan otherwise Home Collateral Personal line of credit (HELOC)

They typically offer large rates than top mortgages because lender assumes on higher risk. In case of foreclosures, the key home loan could be paid down before any second mortgage loans.

However, given that loan is still collateralized, interest levels to own 2nd mortgage loans are often dramatically reduced than normal unsecured debt for example bank cards, playing cards, and you can consolidation money.

Others biggest benefit of next mortgages is the fact at least some of the desire are, to own consumers exactly who itemize, tax deductible. To receive a full income tax work for, the full debt on your family–for instance the household equity loan–do not surpass the marketplace worth of the home. Speak to your income tax mentor for info and you can qualifications.

Are another financial wise?

Before you decide which kind of next home loan is perfect for your, very first know if you really need that. If you have lingering paying products, using the security of your home may not help and may even, in fact, getting detrimental. Wonder another:

- Might you seem to fool around with credit cards to pay for home expense?

- For individuals who subtract your costs from the earnings, can there be a deficit?

- If you decided to pay off creditors by using the security in your home, do truth be told there getting an effective possibility of taking on significantly more unsecured debt?

For folks who replied yes to the of your own preceding concerns, scraping the actual security in your home to pay off user financial obligation may be a preliminary-name service which can place your domestic in danger out of foreclosure.

By using the equity of your house to repay their unsecured debts following run up your handmade cards again, you could find yourself in a really difficult condition: zero domestic equity, large personal debt, and you can an inability and come up with payments towards one another your safeguarded and unsecured financial duties. Investing more than you will be making is never reasonable so you can use the collateral of your property.

How can i start off?

If you have concluded that having fun with house security is practical, your upcoming step would be to understand the procedure for acquiring good 2nd financial and to choose from a property collateral financing and you will a house security personal line of credit.

A few.

A consideration to look at when looking for the next financial are settlement costs, that can tend to be loan situations and you may software, origination, term search, assessment, credit score assessment, notary and judge charge.

Several other decision is whether or not you want a fixed otherwise varying attract rates. If you choose a varying speed financing, find out how far the speed can transform across the life of the borrowed funds incase discover a limit one to tend to steer clear of the price away from surpassing a certain amount.

Annual percentage rate (APR).

Looking around into reasonable Apr (Apr) is actually built-in to getting the most out of your loan. The newest Apr to possess home equity loans and domestic guarantee contours is actually computed differently, and you will alongside reviews is tricky. To own old-fashioned family equity fund, the newest Annual percentage rate comes with activities or other money fees, since Apr getting a house collateral range would depend solely on the periodic interest.

Additional factors.

Prior to making one decision, get in touch with as much loan providers you could and you can evaluate the new Annual percentage rate, closing costs, financing conditions, and you will monthly payments. In addition to inquire about balloon costs, prepayment charges, punitive interest rates in case there is default, and you may introduction out-of borrowing insurance policies.

While looking for money, do not trust lenders and agents who solicit you inquire fellow gurus, natives, and you may relatives to own trustworthy prospects, and check out the Internet having immediately accessible prices.

Family Equity Loans.

With a property guarantee mortgage, might get the profit a lump sum after you romantic the loan. New installment title might be a predetermined several months, generally regarding four so you’re able to 2 decades. Always, the latest fee agenda calls for equal payments that may pay off the whole mortgage contained in this that point.

Specific loan providers ount out-of equity you really have in your home brand new projected worth of the house without any amount you still are obligated to pay. You are not required to borrow the full number but can instead acquire merely what you want.

Interest rates are fixed in the place of adjustable. You could imagine a property equity loan instead of a house security line of credit if you would like a-flat amount to own a particular objective, for example an improvement to your home, or even to pay all of your unsecured debt.

Domestic Collateral Personal lines of credit.

A home equity line are a variety of revolving borrowing from the bank. A specific amount of credit is determined if you take a share of your appraised property value your house and you will subtracting the balance owed towards present home loan. Money, expense, almost every other bills, and you may credit history are situations inside the determining the credit line.

Immediately after recognized, you will be able in order to acquire doing you to restriction. Small print regarding how the money are going to be reached is actually detailed throughout the mortgage data.

Focus is sometimes changeable in place of repaired. Although not, the cost identity is sometimes repaired of course the expression ends up, you’re up against a balloon commission the fresh unpaid percentage of your loan.

The advantage of a property collateral line of credit would be the fact you can remove seemingly short figures sometimes, and notice simply feel billed when you deduct the bucks. The fresh new disadvantage is the enticement to help you costs indiscriminately.

Watch out for too-good-to-be-genuine has the benefit of.

You may be lured because of the offers that allow you to use to 120% of the house’s security. Remember that people appeal above the house’s security maximum was perhaps not tax-deductible. At exactly the same time, you might not have the ability to sell your property until the lien was met, which can negatively change the marketability of your home.

In the end, if you all of a sudden improve your attention, government laws offers three days immediately following finalizing a https://paydayloanalabama.com/auburn/ house security mortgage package so you can terminate the deal for any reason.

No Comments